CompStak: San Francisco Office Rents Continue Their Rise

Re-posted from: The Registry Bay Area Real Estate

By: Robert Carlsen

Date Posted: August 30, 2015

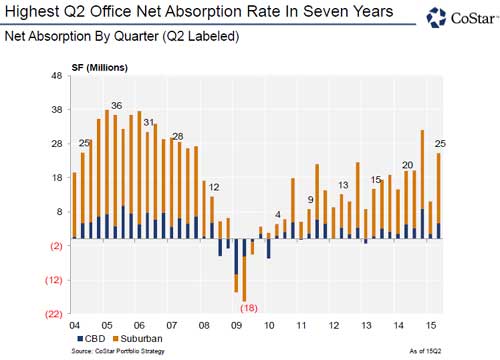

Many brokers, appraisers and developers have experienced San Francisco’s strong first half of the year in commercial real estate, with demand for office space continuing to outpace supply and office rents increasing across all building classes and submarkets.

While Class A and B buildings in San Francisco both had quiet starts to 2015, they recently picked up to close the first half of the year in the black, according to CompStak Exchange, a New York-based commercial real estate database specializing in lease comparables.

CompStak’s second quarter 2015 effective rent report said that Class A effective office rents in San Francisco were up 6.6 percent to $65.29 per square foot over the previous six months and Class B buildings performed even better, with effective rents increasing 12 percent to $59.40 per square foot over the same time period.

And with the tightness of available office space comes the absence of perks. “Landlords who also own property in markets outside of San Francisco know how favorable market conditions really are,” the report said. “Concessions given in San Francisco are far below comparable markets like Los Angeles, Manhattan and Washington, D.C.”

“For example, tenants in Washington, D.C., and Los Angeles County receive, on average, twice as much in free rent and tenant-improvement dollars. The strength of the San Francisco leasing market is evident when viewed in this light.”

According to Blake Toline, a CompStak research analyst, most of the demand driving up prices in San Francisco is coming from technology companies, which has been a trend over the past few quarters. The north and south Financial Districts typically have more corporate tenants, such as law, finance and consulting firms, “but that is starting to change as space around the city becomes harder to find, forcing tech tenants that wouldn’t have normally looked at the central business district to sign space there,” he said.

CompStak said that Class B buildings offer space with more character, unique interiors with exposed brick, operable windows and open floor plans, which makes them more attractive to tech tenants.

Toline provided some recent submarket tenant rent increases over the past six months.

In the lower South of Market area, Class B space is up 3.8 percent to $67 per square foot. Recent lease deals in the region include Elance at 475 Brannan St., which featured an 18,000-square-foot expansion, resulting in an effective rent in the mid-$70s; Hipmunk at 434 Brannan St., which included a 17,000-square-foot short-term renewal and saw effective rents in the high $60s; and HoneyBook at 539 Bryant St., which included a 15,000-square-foot rental in the low $70s.

In the south Financial District, Class A space is up 3.5 percent to $69.80 per square foot. Recent lease deals include WeMo Technologies at 555 Market St., which rented 172,000 square feet in the high $60s; Instacart at 50 Beale St. has 56,000 square feet of lease space in the high $60s; and Intercom at 55 2nd St. has 23,000 square feet of space in the mid-$70s range.

Additionally, in the north Financial District, Class A space is up 5 percent to $65 per square foot. Recent deals include a Sheppard Mullin Richter renewal at 4 Embarcadero, with 72,000 square feet of space in the high $70s; Sentient Technologies at 1 California St., with 17,000 square feet going for the low $70s; and HIG Capital at 1 Sansome, with its 11,000 square feet priced in the low $70s.

Link to article: SF Office Rents Continue Their Rise